Since we launched the Innovative Finance Playbook in November 2022, Catalyze and the Nowak Metro Finance Lab have been assessing Revenue Based Financing, or RBF, as a tool to help address the capital gaps and deficiencies laid bare by the COVID pandemic; namely, the 83% of entrepreneurs who do not access traditional bank debt and venture capital. We recently released a report sharing our findings entitled “The State of Revenue Based Financing and CDFIs.”

The report, informed by Catalyze’s peer group of 10 mission-driven lenders piloting RBF in their portfolios, provides a practical guide for CDFIs and other mission-driven capital providers to develop RBF products. It explores an emerging spectrum of RBF providers, addresses challenges, and offers resources for RBF implementation, all contextualized with case studies of real RBF deals.

Despite the pandemic’s disruptive dynamics, the traditional capital product paradigm has seen little change for decades. Our current capital product landscape – a binary between debt and equity – has put far too many entrepreneurs who cannot access traditional capital between a rock and a hard place, choosing between bootstrapping their businesses with no outside capital at all or relying on unsavory capital products that are inordinately expensive at best, and outright predatory at worst.

Remedying these deficiencies will require capital products, like RBF, which are fit to purpose, provide much-needed flexibility, and offer pathways to sustainable growth. CDFIs – long touted for their ability to serve otherwise hard-to-reach firms – must play a leading role in accelerating the adoption of RBF and the scaling of RBF must be part of a larger wave of financial innovation around products, capital stacks and ecosystems.

A growing movement to fill a glaring gap

Conventional debt and equity products have left a major gap in the small business capital market. Debt, traditionally in the form of term loans, typically comes with a fixed repayment schedule and requires collateral – cash or a physical asset – for approval. While these loans are familiar and consistent, their relative rigidity and asset-based underwriting can make them unattainable for many firms. Equity from outside investors, typically in the form of venture capital, provides flexible capital for growing firms, but is dilutive (i.e., requires the entrepreneur to give up an ownership stake in the company) and can place firms on a never-ending cycle of increasing valuations that is frequently unrealistic. The VC model can be a good fit for asset-light, tech enabled firms, but is typically not an option for the rest.

RBF can help to fill that gap. RBF can be structured as a redeemable equity investment, in which the company buys back the investor’s equity as revenue grows over time, or as a revenue-based loan. In either case, an RBF recipient repays the investment as a share of their revenue, typically 2-5%, until an agreed-upon multiple or cap of the principal amount, typically 1.4-2x, is reached.

RBF provides much-needed flexibility for borrowers and investees by tying repayments to cash flows. Moreover, its underwriting is less reliant on existing asset bases for collateral than traditional lending, making it accessible for asset-light businesses. And with an investment exit built into its structure from the beginning via revenue-based repayments, it provides an alternative to the endless march toward higher valuations and an eventual sale required by venture capital.

Collectively, these features can help RBF make capital more accessible to a wider array of firms than traditional lending and investing products. Seasonal businesses with fluctuating cash flows, asset-light businesses, and growing firms that are not on a venture capital-like trajectory can all benefit.

Industry reports value the global RBF market at $2.8 billion as of 2022, with the U.S. representing a relatively small share. With a few noteworthy exceptions, CDFIs have historically not been part of that market. In recent years, however, RBF has gained momentum among a group of leading CDFIs. Today, Catalyze estimates that approximately 20 CDFIs provide RBF, with more potentially interested going forward.

Catalyze’s peer group of 10 CDFIs and mission-driven lenders captured a snapshot of this evolving market.[1] The group explored RBF strategies and shared best practices on topics like technical assistance, portfolio construction, underwriting, and fundraising. Peer group members who disclosed portfolio data have completed at least 49 deals totaling $4,640,000 as of August 2023, with an expected 145 deals and a budget of $15,690,000 by 2024.

Emerging RBF market segments

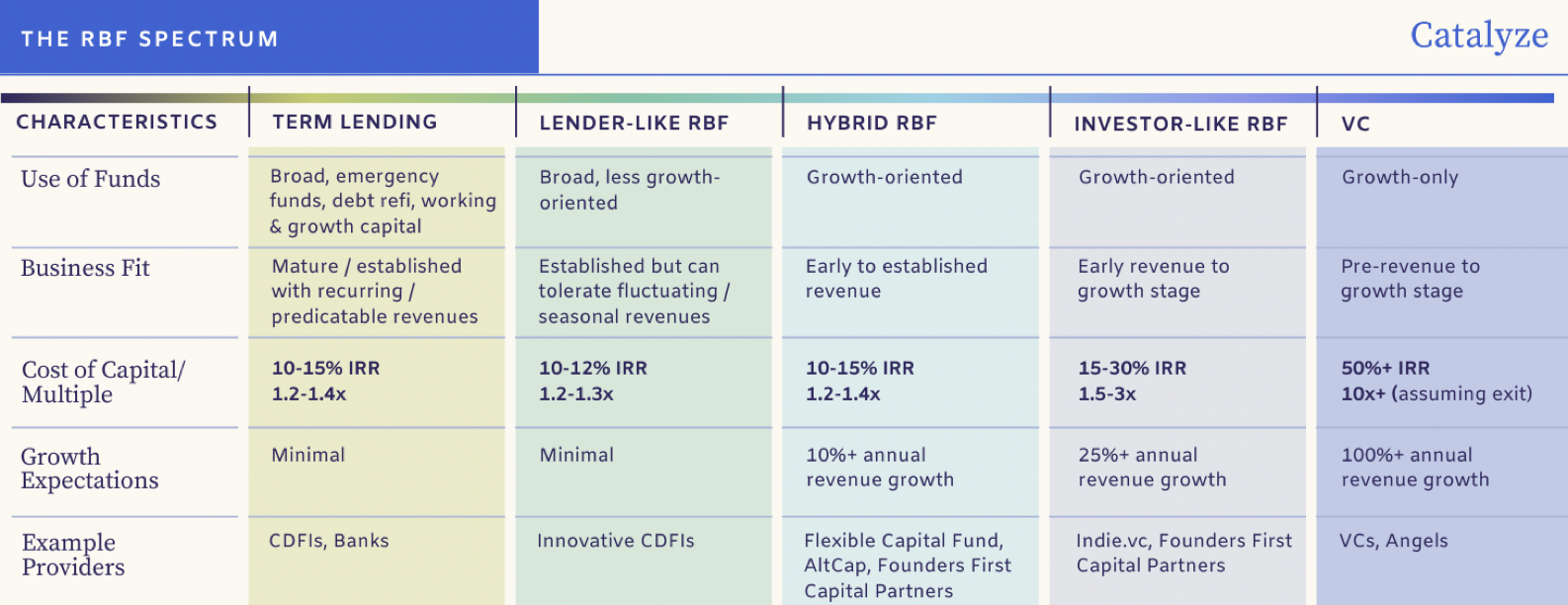

With the increased prevalence of RBF and broad range of approaches represented within the peer group, we now have a clearer idea of the various types of RBF in the market, allowing distinctions between lender-like and investor-like RBF. The spectrum demonstrates how RBF can be suitable for a range of business types, uses and return expectations.

Figure 1: The RBF Spectrum

Lender-like RBF closely aligns with term lending, relying on historical cash flows for underwriting. It tends to favor conservative practices like credit score assessments and tax return reviews. Lender-like RBF offers versatility in the use of funds, provides minimal grace periods, and often considers assets for collateral. While it is more conservative than other forms of RBF, it generally comes with expanded risk tolerance over traditional term loans.

One CDFI member of the peer group used the lender-like RBF approach to help a coffee shop client out of a precarious financial position. With little collateral and an average credit score, the business owner turned to a merchant cash advance (“MCA”) to pay for a $30,000 espresso machine. The MCA’s demands on the business’ cash flows – 15% of all sales – constrained the company’s growth instead of fueling it. A CDFI offered the business an RBF loan to refinance the MCA – underwritten in part based on strong historical financials and margins – in which the business agreed to repay 1.25x the principal amount via a 6% monthly revenue share. The new loan has proven far more sustainable for the business, which is now on a sustainable path to repayment.

More equity investor-like RBF can fund growth-oriented plans without requiring the rapid revenue growth typical in venture capital. It requires high-touch pre- and post-investment support and, given its orientation towards growth, often includes grace periods at the outset. It is more speculative in nature, addressing gaps in high-risk, early-stage growth funding. Accordingly, it is generally more expensive than lender-like RBF.

In one case, a husband-and-wife team recently transitioned their home-based welding hobby into a full-fledged business. With comfortable margins and growing demand for their services, the company quickly needed to expand to a larger facility with more sophisticated equipment. The couple’s personal assets provided insufficient collateral and the company lacked historical financials due to its young age, making a more traditional debt product difficult to access. Based on the company’s business acumen, strong growth prospects, and technical expertise, a local capital provider offered a $32,000 revenue-based investment with a 1.28x cap and 6% monthly revenue share.

In between the two is a hybrid model, incorporating elements of investor-like processes while retaining term loan underwriting policies. It’s apt for contract- and project-based businesses, allowing CDFIs to finance ventures based on secure future revenues to reduce risk. Recipient businesses may lack the collateral or credit score required for a traditional loan but have a robust pipeline of future revenues from contracts or purchase orders. While growth remains the focus for this type of RBF provider, the approach also offers moderate downside protection.

As RBF has grown in popularity and developed a reputation for entrepreneur friendliness, however, providers of less savory products – MCAs in particular – have sought to capitalize on it. RBF and MCAs share some characteristics, namely an up-front influx of capital with future repayments based on cashflows. But there are significant differences between the two. MCAs draw repayments daily or weekly, are intended to be repaid within a very short time period (less than one year), may require confessions of judgments, and can lead to vicious debt cycles. RBF is typically longer-term capital to fuel growth over three to five years. Repayments are monthly (not daily or weekly) based on a negotiated revenue share, and capital is often paired with hands-on business support.

Going forward

The paper should inform CDFIs, policymakers, and business support organizations looking to expand access to capital by adding RBF to their capital toolkits. While RBF is still in a nascent stage among CDFIs, four signals will indicate progress towards a more mature market as its uptake accelerates.

New metrics: Lenders and policymakers must understand the outcomes of RBF as a financial product, especially relative to the status quo options of term lending and VC. Mission-driven lenders see RBF as a tool to achieve additional impact outcomes – primarily, expanded access to capital – beyond returns-oriented objectives. Outcomes to track as RBF use increases include accessibility for different demographic groups, availability of capital for firms that otherwise may not qualify for more traditional products, and the growth and financial health of recipient businesses.

Increased clarity and industry standards: There is currently no clear guidance on tax and accounting treatment for RBF, leaving it in something of a gray area. Our report details how RBF practitioners are dealing with this uncertainty in varying ways. Further, existing fair lending and borrower protection standards rely heavily on APR tests to determine whether a product is borrower-friendly or usurious. Given RBF’s more flexible repayment structure and lack of a standard APR, it does not fit well within such standards. Updated and more definitive guidance on both areas can help accelerate RBF adoption.

Continued innovation from an array of leading organizations across domains: Catalyze’s peer group demonstrated how RBF lenders and intermediaries have innovated to use the RBF approach in distinct ways. We expect to see continued innovation from early-mover CDFIs as they increasingly use RBF.

Support functions like legal and accounting support and technology will provide critical market infrastructure to move RBF into the mainstream. Law firms like RPCK Rastegar Panchal, accounting firms like Dark Horse CPAs, and technology platforms like Ned have proven to be invaluable for leading-edge RBF providers. We expect continued maturation in these functions with time and increased RBF volume.

Additional support from capital providers to help test and codify RBF: Philanthropy has been an important player in capitalizing RBF initiatives. Members of the peer group have received support from organizations like the Kauffman Foundation, Common Future, Boston Children’s Hospital, and the Colorado Health Foundation, among others. Publicly-supported small business programs can also increase capital availability. In the State Small Business Credit Initiative, for instance, Washington state’s Revenue Based Loan program and Business Oregon’s Royalty Fund can serve as early test cases of RBF’s applicability.

Small businesses play an indisputably significant role in the U.S. economy, but our capital product landscape has failed to serve far too many of them. Increased adoption, innovation, and maturation of RBF among mission-driven capital providers can provide an additional tool to help fill this long-standing product gap.

Bruce Katz is the Founding Director of the Nowak Metro Finance Lab at Drexel University. Bryan Fike is a Research Officer at the Nowak Lab. Michael Belles is a Co-Founder and Innovative Finance Manager at Catalyze.

[1] Peer group members include AltCap, Allies for Community Business, Community Investment Corporation, Community Reinvestment Fund, Denkyem Co-op, Grow America, Lendistry, LISC, the Tucson Industrial Development Authority, and WEPOWER.