After nearly fifteen years of robust rent growth, many renters across the country are finally seeing something unimaginable a few years ago: rent relief. According to CoStar, U.S. apartment rents after concessions are approximately flat on a year-over-year basis. Out of the approximately 200 markets tracked by CoStar with more than 100,000 households, over one-third have experienced declining rents with most of these markets concentrated in 10 sunbelt and mountain region states.

A range of market types are emerging in the country, which have implications not only for developers and investors but also for broader public responses. In this piece, we boil down the variance across the country to two admittedly broad market types – Supply Growth Metros and Supply Stagnant Metros – to illustrate the different policy responses that align with market dynamics.

Supply Growth Metros

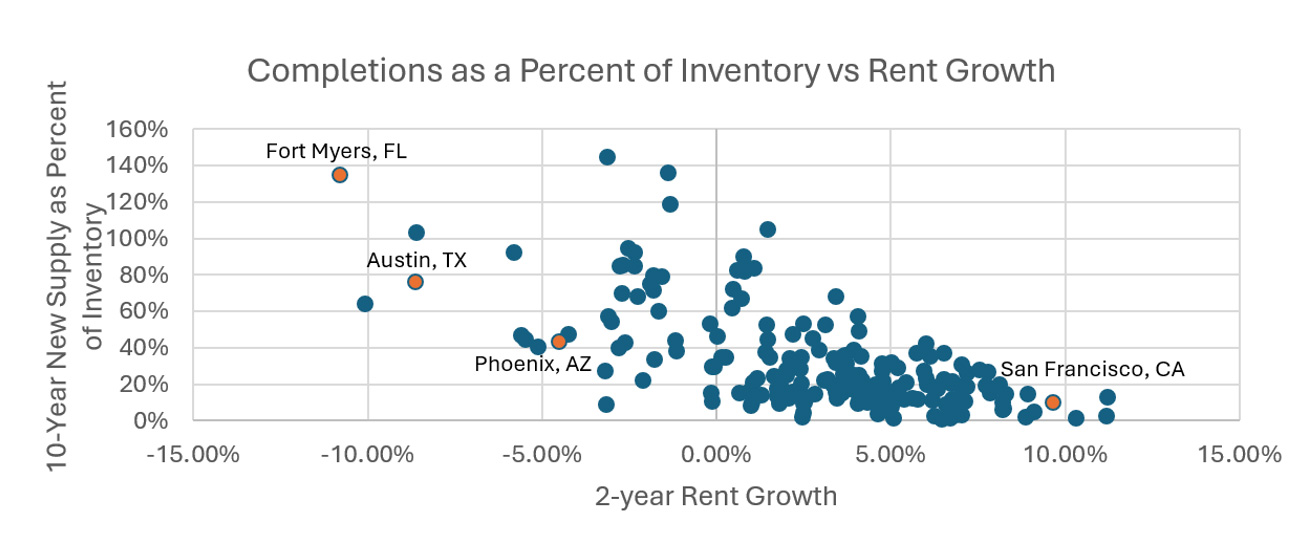

Perhaps unsurprisingly, markets experiencing rent softness have one thing in common: a surge in new supply. Over the past decade, markets exhibiting recent rent declines saw inventory grow by more than 50% on average – over twice the pace of markets currently exhibiting rent growth. Despite strong population growth, 36 of these major markets now have vacancy rates above 8 percent with many major markets like Austin, Dallas, Houston, Pheonix and Denver, seeing vacancy rates above 12 percent.

Higher vacancy rates are doing what markets do best: pushing landlords to compete for tenants by reducing rents. As noted in the graph below, markets that experienced significant increase in supply over the past ten years, (measured as a percent of 2016 inventory) have seen some of the largest rent declines over the past two years. In short, rent growth has exhibited a negative correlation with new supply.

Source: Costar, Q4 2025 Data (source date: March 2026)

In Phoenix, some luxury two-bedroom apartments twenty-five minutes west of the city now rent for $1,550 per month (before two months of concessions). Luxury apartments in some pockets of Phoenix are now affordable to households making 60% of area median income), indicating that two people earning $17 per hour can afford to live in a new home located in a strong school district.

Indeed, as some recent articles have highlighted, higher income renters have been a larger beneficiary of this supply as most of the supply has been concentrated amongst luxury apartments. During the past 2 years, average rents for 4-&-5-star apartments in the markets exhibiting declining rents are down 3.8% compared to a 0.9% decrease for 1-& 2-star (naturally affordable) apartments. Out of the markets exhibiting rent declines over the past years, about half saw naturally affordable housing (1-&-2 star) rents also decline. Without this supply, it’s likely that naturally affordable housing rents would be much higher.

While the affordability story has been great for many renters, flat to negative rent growth and persistently high interest rates have pushed developers to face a more medium-term reality: many projects are worth less than construction costs and may require additional equity to refinance construction loans.

As development profits become thin (or negative), multifamily units under construction are down nearly 50 percent nationally from their 2022 peak and 100 percent in many major markets. Given the shift in development capital markets, it won’t take long for the affordable supply tailwind to turn into headwinds.

A Playbook for Maximizing Public ROI in Supply Growth Metros

As we discussed in our prior article, affordable housing players have a historic opportunity to keep homes affordable by providing rescue capital to developers at risk of losing projects to pending loan maturities. With many construction loans coming due requiring equity infusions, public housing authorities and affordable housing funds continue to have a sizable opportunity to directly acquire or provide concessionary capital to incentivize private operators to convert market rate units to long-term affordable homes. These investments can lock in long-term affordability for the lowest income renters often at a fraction of replacement cost. Importantly, many housing authorities such as HACLA in Los Angles and Philadelphia Housing Authority are successfully implementing this strategy.

Indeed, at a time when state and city budgets are stretched from federal uncertainty and loss of commercial property tax revenue, finding capital for affordable housing investments is not an easy feat. One off transactions should be celebrated, but scalability should be the underlying goal. The key to scaling affordable housing investments is identifying the minimum amount of public capital needed to unlock the lowest-cost private capital. Tax-exempt bond financing and property tax abatements can deliver some of the lowest-cost federal and municipal concessionary capital, maximizing public return on investment (ROI).

Supply Stagnant Metros

While this strategy sounds like a win for many affordable housing players, it is a little more challenging to replicate in dense markets with low vacancy rates and rising rents such as Boston, San Francisco or New York City. What many of these markets have in common is very little land for the least expensive construction typology: stick built surface parked multifamily. From the public sector’s perspective, the challenge in these markets is that rising cap rates (causing values to decline) have made market rate development margins too thin to raise institutional equity at scale. Thus, with very little supply in the pipeline, these markets are far from being overbuilt and yet not cheap enough to warrant rescue capital investments that could incentivize market-to-affordable conversions.

A Playbook for Maximizing Public ROI in Supply Stagnant Metros

In supply stagnant metros, the public sector needs to be focused on providing cost-effective financial incentives that unlock more development equity to increase supply. While subsidized debt or equity is helpful, cities stretched for cash should continue to lean on tax incremental financing (TIF) to increase development margins. TIFs can be one of the most efficient tools of concessionary capital because they don’t require upfront concessionary capital –they just reduce tax on the incremental assessed value.

Indeed, while tax abatements on new construction don’t require cash up front, they do have the potential to strain city and state budgets. As noted in a UMass Dartmouth working paper, The Costs and Hidden Benefits of New Housing Development in Massachusetts, the extent of these costs vary based on a neighborhood’s marginal cost to service residents living in new homes. This creates an opportunity for cities to maximize public ROI by identifying TIF areas with excess school and public infrastructure capacity.

To better understand the potential cost of property tax incentives cities should survey neighborhoods to understand which areas may be able to support more housing without much additional cost. Thinking at the state and regional level can also be an effective way to maximize public subsidies. For example, in Boston, inner ring towns like Lynn and Revere have been effective at delivering less expensive housing as land costs often support less dense construction typologies such as 5-story wood frame over concrete or steel towers. States allocating concessionary capital for housing could reimburse transit-oriented commuter cities with available infrastructure capacity for property tax concessions that subsidize lower-cost development areas.

Key Takeaways

As the U.S. multifamily cycle becomes increasingly decoupled across markets, cities and states have the ability to tailor policy interventions that maximize public ROI for varying market cycles. With nearly a third of the U.S. markets over 100,000 households seeing rents decline, affordable housing players have a unique opportunity to make naturally affordable housing permanently affordable. By providing rescue capital to distressed developers, cities can incentivize developers to deed restrict units to affordability levels often at a significant discount to new construction. Understanding the cheapest source of capital for each piece of risk in the capital stack, such as tax-exempt bond financing is critical to making these programs scalable.

Outside of oversupplied markets, many affordable housing actors face structural disadvantages in tackling the affordability crisis. In addition to burdensome zoning and permitting processes, many of these markets are too dense to support less expensive construction typologies seen in the sunbelt. Utilizing tools like tax abatements and TIF will continue to be the key to unlocking much needed development equity. To offer these incentives at scale, cities need to be strategic with their resources, allocating tax subsidies that have the lowest marginal cost of capital. Doing so will require extensive local and regional audits to understand the interdependence of urban infrastructure systems.

As cities and states look to solve their affordable housing crisis, it will be critical that they continue to work together and in-line with federal government to develop solutions that are aligned to disparate market dynamics and policy contexts.

Bruce Katz is the Founder of New Localism Associates and a Senior Advisor to the National Housing Crisis Task Force; Andrew Gibbs is a Managing Director at Arctaris Impact Investors, an impact fund manager focused on affordable and workforce housing investments.